50/30/20 Rule Explained: Simple Budget Method

Best for: Beginners choosing a simple budgeting method (not full budget setup)

💡 Quick Answer: The best budgeting method for beginners is the 50/30/20 rule because it keeps money management simple, clear, and easy to follow.

- ✔️ Divides your income into needs, wants, and savings

- ✔️ Eliminates the need for complex tracking

- ✔️ Helps you balance spending and saving easily

- ✔️ Creates a sustainable system you can stick to long-term

📘 In This Guide 👇

- Best Budgeting Method for Beginners (Quick Decision Guide)

- What Is the 50/30/20 Budget Rule?

- What Makes a Budgeting Method Ideal for Beginners?

- The Structure of the 50/30/20 Rule

- How to Use the 50/30/20 Rule (Practical Beginner Guide)

- Why the 50/30/20 Rule Wins for Beginners

- Pros and Cons of the 50/30/20 Budget Rule

- How It Compares to Other Budgeting Methods

- What If You Can’t Reach 20% Savings Yet?

- Beginner Budget Examples (Simple Breakdown)

- Who Might Need a Different System?

- Why This Method Builds Long-Term Financial Discipline

- Is the 50/30/20 Rule the Best Budgeting Method for You?

- Frequently Asked Questions

- Final Thoughts: Keep Budgeting Simple and Sustainable

Best Budgeting Method for Beginners (Quick Decision Guide)

If you're trying to choose the best budgeting method as a beginner, you don’t need dozens of options. You need one system that is simple enough to start today and flexible enough to stick with long term.

The 50/30/20 rule stands out because it removes complexity and gives you a clear structure without requiring detailed tracking or advanced financial knowledge.

Instead of building a full budget from scratch, this method helps you organize your money into three simple categories so you can take action immediately.

If you want a complete step-by-step system for building your full budget, read:

👉 Need a full budgeting system? Follow our complete monthly budgeting guide.

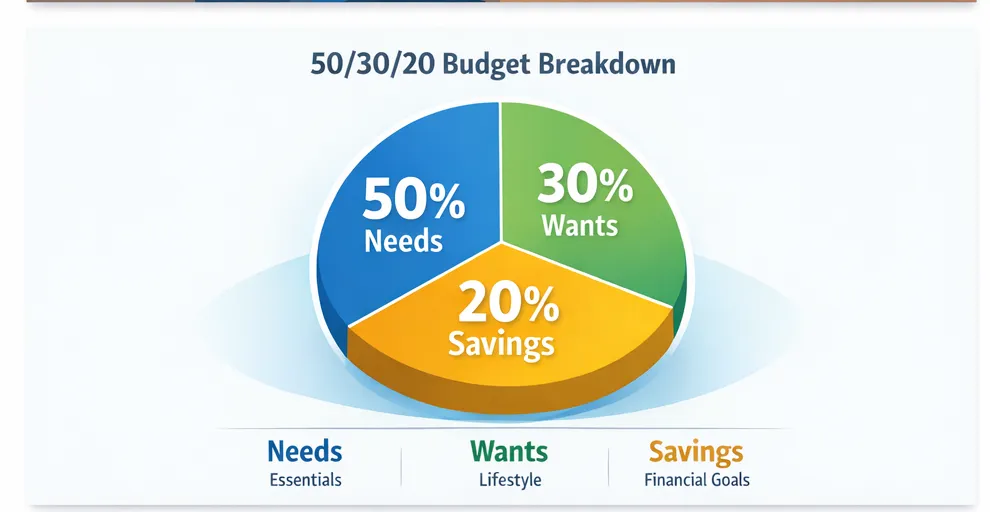

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting method that divides your after-tax income into three categories:

- 50% for needs – essential expenses like rent, food, and bills

- 30% for wants – lifestyle spending such as entertainment and dining

- 20% for savings – savings, investments, and debt repayment

This budgeting method is ideal for beginners because it simplifies money management, reduces overspending, and helps build consistent saving habits without complex tracking.

This guide is based on proven budgeting systems used by financial counselors, nonprofit credit agencies, and long-term savers around the world.

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people, especially those building stability from limited income.

What Makes a Budgeting Method Ideal for Beginners?

Before calling any budgeting system “the best,” it’s important to first understand what beginners truly need.

A great starter budgeting method should be simple enough to grasp in minutes, without requiring complex calculations or financial jargon. It shouldn’t demand excessive tracking that quickly becomes overwhelming. Instead, it should offer flexibility allowing you to adjust when your income changes or unexpected expenses arise.

Most importantly, a beginner-friendly budget should naturally build saving habits into your routine and feel realistic to maintain. If a system feels too strict or complicated, people abandon it not because they lack discipline, but because the method isn’t sustainable.

Many budgeting strategies fall short in one or more of these areas.

The 50/30/20 rule doesn’t.

If you want full control of your finances, follow a complete monthly budgeting system.

The Structure of the 50/30/20 Rule

The 50/30/20 rule was popularized by Harvard bankruptcy expert Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, where she introduced this balanced percentage-based budgeting system.

- 50% for Needs – Essential expenses such as rent, utilities, groceries, transportation, insurance, and minimum debt payments.

- 30% for Wants – Lifestyle choices like dining out, entertainment, subscriptions, travel, and hobbies.

- 20% for Savings – Building financial security through emergency funds, investments, retirement contributions, or extra debt repayments.

That’s the entire structure.

Get Started with Budgeting Without Overthinking

If you're just starting, these tools help you take action quickly. No complicated setup, just a clear way to organize your money and begin building better habits.

✔ Simple expense layout

✔ Perfect for beginners

✔ Visual money tracking

✔ Great for discipline

✔ Builds consistency

✔ Beginner-friendly system

There are no complicated spreadsheets with endless expense categories.

No exhausting daily tracking.

No financial expertise required.

Just three straightforward “buckets” that create clarity, balance, and control over your money.

Now, let’s take a closer look at how each category works in practice.

How to Use the 50/30/20 Rule (Practical Beginner Guide)

This structured approach shows exactly how to apply the 50/30/20 rule in real life without feeling overwhelmed.

- Calculate your monthly after-tax income

- List all essential expenses (needs)

- Track your lifestyle spending (wants)

- Set a savings goal (start with 10–20%)

- Adjust your spending to fit the 50/30/20 structure

This process turns the 50/30/20 rule from a concept into a system you can apply immediately.

1. 50% for Needs: Cover Your Essentials

This category covers your essential expenses, the non-negotiables that keep your life stable and functioning.

If your fixed expenses feel too high, learn how to reduce monthly expenses without sacrificing essentials.

These are the costs that protect your basic security and quality of life, including:

- Rent or mortgage

- Utilities (electricity, water, internet)

- Groceries

- Transportation

- Insurance

- Minimum debt payments

If these bills go unpaid, the consequences are serious; housing instability, service disconnections, damaged credit, or mounting penalties.

Setting a 50% guideline for needs creates powerful financial awareness. If you discover that your essentials consume 70–80% of your income, that isn’t a personal failure, it’s valuable insight. That clarity helps you make informed decisions: either reduce certain expenses or find ways to increase your income.

Awareness is the first step toward control, and this structure makes that awareness immediate and actionable.

Struggling with high essential expenses? Read: how to budget on a low income to regain control.

2. 30% for Wants: Enjoy Life Without Guilt

This is where the 50/30/20 rule becomes psychologically powerful.

Many beginner budgets fail because they remove enjoyment completely. But that’s not discipline; it’s deprivation. And deprivation often leads to impulsive “rebound” spending that derails progress.

The 30% category intentionally makes room for lifestyle choices such as:

- Dining out

- Streaming services

- Shopping

- Hobbies

- Gym memberships

- Travel

By deliberately allocating money for enjoyment, the system removes guilt from spending.

You’re not “breaking” your budget.

You’re following it.

That subtle mental shift makes a significant difference. Instead of feeling restricted, you feel balanced. And when a budget feels balanced, consistency becomes much easier to maintain which is what ultimately drives long-term financial success.

If overspending is your biggest issue, see: how the envelope system controls spending.

3. 20% for Savings: Build Your Financial Future

This category is the true game changer.

The 20% portion is dedicated to building your financial future, including:

- Emergency funds

- Retirement contributions

- Investments

- Extra debt repayment

Not sure how to grow your savings? Start with: practical ways to save money consistently.

Rather than saving whatever happens to be “left over” at the end of the month, this method treats saving as a priority, just like rent or utilities. It becomes a fixed commitment, not an afterthought.

That simple shift changes everything.

Saving moves from optional to automatic. And when saving becomes automatic, progress no longer depends on willpower or mood. Over time, consistency compounds and that steady discipline builds wealth far more reliably than bursts of motivation ever could.

Reduce Manual Tracking and Improve Accuracy

Once you’ve started budgeting, these tools help you streamline your system, reduce manual tracking, and gain a clearer, more accurate view of your finances.

✔ Monthly tracking system

✔ Clear financial overview

If you don’t yet have a simple tracking system, follow our complete beginner budgeting guide to see where your money is leaking and how to plug those holes.

What is the 50/30/20 rule in simple terms?

The 50/30/20 rule is a budgeting method that splits your income into needs (50%), wants (30%), and savings (20%). It helps you manage money easily without tracking every expense.

Is the 50/30/20 rule the best budgeting method for beginners?

Yes, the 50/30/20 rule is one of the best budgeting methods for beginners because it is simple, flexible, and easy to follow without detailed financial planning.

How do I start the 50/30/20 rule?

To start, calculate your after-tax income, divide it into the three categories, and adjust your spending so it fits within the 50/30/20 percentages.

What if I can’t save 20% of my income?

If saving 20% is difficult, start with a lower percentage like 10% and increase it gradually as your income grows or expenses decrease.

Why the 50/30/20 Rule Wins for Beginners

1. It Reduces Decision Fatigue

Traditional budgeting often demands constant micro-decisions:

- “How much should I allocate for groceries?”

- “Are my subscriptions getting out of hand?”

- “Did I overspend in my entertainment subcategory?”

Over time, this level of detail becomes mentally exhausting. The more decisions you have to make, the easier it is to feel overwhelmed and eventually give up.

The 50/30/20 rule removes that complexity, making it a practical budgeting system that beginners can follow without constant stress.

Does this expense fall under Needs, Wants, or Savings?

That clarity reduces decision fatigue. And when budgeting feels simpler and less stressful, you’re far more likely to stick with it. Consistency not perfection is what drives real financial progress.

2. It Balances Discipline and Flexibility

Some budgeting systems are overly rigid. Others are so loose that they provide little real guidance.

The 50/30/20 method strikes a healthy balance between the two.

It offers enough structure to prevent financial chaos, yet enough flexibility to adapt to real life. You’re guided by clear percentages, but you’re not trapped by dozens of restrictive rules.

If your income increases, the percentages scale automatically, meaning your savings grow along with your earnings.

If your expenses shift, you can adjust within each category without rebuilding your entire budget.

In other words, the system is firm but forgiving. It provides direction without pressure and that balance is what makes it sustainable over time.

3. It Prevents Burnout

When starting out, many beginners fall into one of two extremes:

- They save nothing at all.

- Or they try to save 40–50% immediately, feel overwhelmed and quit within weeks.

Both approaches are unsustainable.

The 50/30/20 rule avoids these extremes by creating steady, realistic momentum. Saving 20% is ambitious enough to make meaningful progress, yet balanced enough to maintain alongside everyday living.

It promotes progress without pressure. Growth without burnout.

And in personal finance, consistency will always outperform short bursts of intensity. Small, steady actions repeated over time build far stronger results than aggressive efforts that can’t be maintained.

4. It Works at Almost Any Income Level

If your income is currently limited, consider increasing it with realistic side income ideas for beginners.

Whether someone earns $800 or $8,000 per month, the percentages remain the same only the amounts change.

That built-in scalability makes the 50/30/20 rule universally practical. It adjusts naturally to different income levels without requiring a completely new system.

Because it’s based on proportions rather than fixed figures, the method works for students, young professionals, families, and high earners alike.

In the end, it’s not income-dependent, it’s behavior-dependent. And strong financial behavior, applied consistently at any income level, is what drives lasting stability and growth.

Want a Complete Budgeting System?

This method is your starting point. To fully organize your finances step-by-step, follow our full guide: Build Your Monthly Budget

Pros and Cons of the 50/30/20 Budget Rule

Pros

- Simple and beginner-friendly

- No complex tracking required

- Builds consistent saving habits

- Flexible and adaptable to different incomes

Cons

- May not work well with very low income

- Less detailed than advanced budgeting systems

- Requires discipline to stick to percentages

Choose the Right Budgeting Tool for Your Style

| Product | Best For | Ease of Use | Action |

|---|---|---|---|

| Budget Planner Book | Beginners | Very Easy | View |

| Envelope System Kit | Spending Control | Easy | Check Price |

| Budget Binder | Full Organization | Moderate | View |

How It Compares to Other Budgeting Methods

Other budgeting systems aren’t bad, many are detailed and effective. The difference is that they often require more time, stricter tracking, and greater discipline.

This article focuses on choosing the right method. If you want to actually build and implement a full budget step-by-step, go here: how to create a monthly budget.

For beginners, that level of complexity can feel overwhelming and difficult to sustain. The challenge isn’t that these systems don’t work, it’s just that they demand more effort than most people are ready to commit at the start.

Zero-Based Budgeting

In this approach, every dollar is given a specific role before the month even begins. Nothing is left unassigned; each amount is intentionally directed toward a defined purpose.

The method is highly detailed and can be extremely effective for maintaining tight financial control. However, for beginners, the level of planning and ongoing tracking required can feel time-consuming and mentally demanding.

While powerful, it often requires more structure and commitment than someone just starting out may be ready to manage.

Envelope System

This method uses physical cash envelopes for different spending categories. Each envelope holds a fixed amount, and once the cash is gone, spending in that category stops.

It can be especially powerful for people who struggle with overspending, as physically seeing and handling cash creates strong spending awareness and discipline.

However, in today’s digital-payment world where most transactions happen through cards, transfers, and online platforms, maintaining a strictly cash-based system can be inconvenient and harder to manage consistently.

Aggressive Savings Models

This approach is designed to accelerate wealth building as quickly as possible. It often encourages aggressive saving and strict spending limits, which can be highly motivating for those ready to move fast.

However, at the beginner stage, such intensity can feel unrealistic and difficult to sustain. When expectations are too high too soon, frustration can replace motivation.

For most people starting their financial journey, simplicity is more powerful than perfection. A system that is easy to follow and maintain will always outperform one that looks impressive but proves exhausting over time.

If you’re starting from zero, read our guide to building savings from zero to strengthen your financial foundation.

Budgeting Methods Comparison Table

| Method | Complexity | Best For | Beginner Friendly? |

|---|---|---|---|

| 50/30/20 Rule | Low | Balanced financial growth | Yes |

| Zero-Based Budgeting | High | Detailed expense control | Moderate |

| Envelope System | Medium | Overspending control | Yes (Cash users) |

For those who prefer more precision and control, zero-based budgeting assigns every dollar a specific purpose.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

What If You Can’t Reach 20% Savings Yet?

That’s completely normal.

If your current breakdown looks like:

- 60% Needs

- 30% Wants

- 10% Savings

you’re not failing, you’re building awareness and discipline.

Financial progress rarely begins with perfect numbers. It begins with understanding where you stand. From there, you can make gradual adjustments as your income increases or your expenses decrease.

Start where you are. Improve step by step.

The objective isn’t instant perfection. It’s steady, sustainable improvement that compounds over time.

If your income is tight, learn realistic ways to increase your income so you can improve your savings rate.Beginner Budget Examples (Simple Breakdown)

Let’s assume your monthly take-home income is $1,000.

Using the 50/30/20 framework, it would be allocated as follows:

- $500 → Needs

- $300 → Wants

- $200 → Savings

Likewise, if you earn $2,000 monthly:

- $1,000 → Needs

- $600 → Wants

- $400 → Savings

Rather than monitoring 15 or 20 separate spending categories, your focus is simply to ensure each major bucket stays within its limit.

This approach provides clear financial boundaries without overwhelming detail. You maintain structure and direction, but without the pressure of constant micro-tracking.

It’s disciplined, yet manageable. Structured, but not suffocating.

Who Might Need a Different System?

The 50/30/20 rule isn’t perfect for every situation.

It may be less suitable if:

- Your income fluctuates significantly from month to month

- Your essential expenses already consume 70% or more of your income

- You’re carrying high-interest debt that requires an aggressive repayment plan

In these cases, a more customized or temporary strategy may be necessary to stabilize your finances first.

However, for the average beginner seeking clarity, structure, and better control over their money, this method provides a strong and practical starting point. It simplifies decision-making, encourages balanced progress, and builds foundational financial habits that can be refined over time.

Why This Method Builds Long-Term Financial Discipline

Budgeting isn’t about restriction, it’s about awareness. It’s about knowing where your money goes and making intentional choices that align with your priorities.

The 50/30/20 rule is effective because it focuses on what truly matters. It:

- Simplifies everyday money decisions

- Encourages saving as a built-in habit

- Allows room for enjoyment without guilt

- Builds financial confidence step by step

Beginners don’t need complicated spreadsheets or rigid rules. They need a system that feels manageable and sustainable.

Because real progress doesn’t come from short bursts of discipline, it comes from momentum. And momentum is built through a method you can consistently follow beyond the first 30 days.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

Is the 50/30/20 Rule the Best Budgeting Method for You?

If you're new to personal finance, this percentage-based budgeting strategy provides structure without complexity. It teaches balance, builds savings automatically, and prevents burnout.

For most beginners, it is the best budgeting method to start with because it prioritizes sustainability over perfection.

Frequently Asked Questions

Yes. It is simple, flexible, and easy to maintain without complex tracking.

This is common. Focus on gradual adjustments and increasing income where possible.

Yes. The 50/30/20 rule is a guideline, not a strict law.

Yes, but adjustments may be necessary. If essential expenses exceed 50%, you can temporarily use a 60/30/10 split while working to increase income or reduce costs.

For beginners, the 50/30/20 rule is easier to maintain because it focuses on broad categories rather than assigning every dollar a specific job.

Build a Complete Budgeting System That Scales

If you're ready to take full control of your finances, these systems combine tracking, planning, and goal-setting into one structured approach.

✔ Savings + expense tracking

✔ High discipline tool

✔ Long-term tracking

✔ Better financial clarity

Final Thoughts: Keep Budgeting Simple and Sustainable

The best budgeting method for beginners isn’t the most detailed or sophisticated.

It’s the one you can understand today and still be confidently using six months from now without feeling overwhelmed.

The 50/30/20 rule delivers that balance. It provides:

- Structure without rigidity

- Discipline without burnout

- Simplicity without confusion

It gives you a clear starting point without unnecessary complexity.

Start here.

Build the habit.

Refine as you grow.

Ready to Apply This Budgeting Method?

Ready to turn this method into a complete system? Follow our step-by-step guide: Build Your Full Budget System

Your financial journey doesn’t need to begin with perfection. It simply needs to begin with consistency, because consistent action, over time, is what turns small steps into lasting progress.

This content is for educational purposes only and does not constitute financial advice.