How to Create a Monthly Budget That Actually Works

Written and Reviewed by SmartMoneyTrek Financial Research Team | 10 minute read.

📘 In This Guide 👇

- Introduction: Budgeting Is Not Restriction — It Is Direction

- What a Monthly Budget Really Is

- Why You Need a Monthly Budget — No Matter Your Income Level

- The Real Reasons Most People Fail at Budgeting

- How to Create a Realistic Monthly Budget Plan (Beginner-Friendly System)

- The 50/30/20 Budget Rule (Balanced Framework)

- Free Budget Kit

- Zero-Based Budgeting: Giving Every Dollar a Job

- Digital vs Manual Budgeting: Which Is Better?

- A Real-Life Example

- How to Stick to Your Budget Long-Term

- When Your Budget Breaks

- Frequently Asked Questions

- Final Thoughts: Your Money Should Serve Your Life

Introduction: Budgeting Is Not Restriction — It Is Direction

Most people hear the word budget and immediately feel tense. It sounds restrictive. It feels like being told “no.” It brings up images of cutting every pleasure, tracking every penny, and living a joyless financial life.

But here is the truth no one explains clearly:

A budget is not a limitation, it is actually a deliberate plan that creates financial freedom.

If you are struggling with day-to-day expenses, start with our realistic ways to save money on a low income to create breathing room before building your budget.

When you don’t have a budget, your money controls you.

When you do, you control your money. The control brings something priceless: peace of mind.

This guide will show you in simple, practical, human terms, how to create a monthly budget that fits your real life, not a perfect imaginary one. You don’t need a finance degree. You don’t need to be rich. You only need a willingness to look at your money honestly and tell it where to go.

This step-by-step guide shows you exactly how to create a monthly budget from scratch, even if you have no prior budgeting experience.

How to Create a Monthly Budget (Quick Answer)

To create a monthly budget that actually works, follow these simple steps:

- Calculate your real monthly income after tax

- List all fixed expenses like rent and bills

- Track your variable spending (food, transport, etc.)

- Set aside money for irregular expenses

- Separate needs from wants

- Adjust spending so it does not exceed your income

This simple system helps you take control of your money, reduce stress, and build savings consistently.

If you want a simple tool to start your budget immediately, this is what most beginners use:

- ✔ Easy monthly layout

- ✔ Tracks spending clearly

- ✔ Perfect for beginners

Who This Monthly Budget Guide Is Designed For

- Beginners who have never budgeted before

- People living paycheck to paycheck

- Anyone trying to pay off debt faster

- Earners who want structured financial control

What a Monthly Budget Really Is (And What It Is Not)

Let’s remove the fear right away. A budget is simply a plan for how you will use the money you already earn. That’s it!

It is not:

- A punishment

- A list of things you’re not allowed to do

- A sign that you are broke

- A tool only for “bad with money” people

Think of your budget as a GPS for your financial life.

When you get into a car and turn on your GPS, it doesn’t judge you. It doesn’t care if you missed a turn. It simply shows you where you are and how to get where you want to go.

Your budget works the same way.

It tells your money:- Where to go

- What to do

- What matters most

Without a budget, money leaks quietly through small decisions: snacks, subscriptions, impulse buys, forgotten charges. With a budget, every dollar has a purpose. A good budget gives you clarity, confidence, and control, especially when combined with smart habits from our proven ways to cut expenses and build savings .

Why You Need a Monthly Budget — No Matter Your Income Level

According to research from the Federal Reserve's Survey of Household Economics and Decisionmaking . The Federal Reserve reports that nearly 37% of adults would struggle to cover an unexpected $400 expense without borrowing or selling something. A structured monthly budget directly reduces this financial vulnerability.

Fact: Research consistently shows that people who follow a written budget are more likely to build savings, avoid debt, and achieve long-term financial stability.

“I don’t earn enough to budget.”

Others say:

“I earn too much to worry about budgeting.”

Both are wrong. A budget helps you:

- Stop living paycheck to paycheck

- Save without stress

- Avoid money surprises

- Pay off debt faster

- Sleep better at night

Without a plan, money disappears. With a plan, money works for you. Budgeting is not about limiting your life, it is about protecting your future.

The Real Reasons Most People Fail at Budgeting

Behavioral finance studies show that people who track spending weekly are significantly more likely to stay within financial targets compared to those who review monthly or less.

People don’t fail because budgeting is hard. They fail because they were taught the wrong way.

Here are the biggest mistakes beginners make:

1. Being Too Extreme

They try to cut all fun, all treats, all enjoyment. That never lasts.

2. Forgetting Irregular Expenses

Car repairs. Birthdays. School fees. Holidays. Annual subscriptions. These costs are real even if they don’t come every month. Ignoring them is why so many “good budgets” suddenly fall apart.

3. Making the Budget Too Complicated

If you need 30 categories and five apps to track your spending, you will quit. Simple beats perfect.

4. Quitting After One Bad Month

A budget is not something you “get right.” It is something you get better at. Progress matters more than perfection.

How to Create a Monthly Budget Step by Step (Beginner-Friendly Plan)

Step One: Know Your Real Monthly Income

Before you can tell your money what to do, you need to know how much you actually have. This is not your salary before tax. This is what actually arrives in your bank account. If your income changes from month to month, use the lowest recent month. That keeps you safe. This number is the foundation of your entire financial plan.

If your numbers reveal a consistent income gap, the solution is not panic, it is strategy. Review our structured guide on high-impact ways to increase your monthly income to close the gap intelligently.

Step Two: List Your Fixed Expenses

These are the bills that do not change much:

- Rent or mortgage

- School fees or subscriptions

- Internet and phone

- Insurance

- Minimum loan/debt repayments

These are your financial “anchors.” They must be paid.

Step Three: Track Your Variable Spending

This is where most money disappears:

- Food

- Transport

- Shopping

- Eating out

- Data plans

- Subscriptions

- Entertainment

If food, transport, and subscriptions are eating your paycheck, use our step-by-step expense cutting guides to bring these numbers under control.

Look at the last two or three months of bank or wallet activity.

Be honest. The numbers don’t judge, they simply reveal.

Example: Monthly Expense Tracking

This simple example shows how to write down and organize your daily spending so nothing slips through the cracks.

Step Four: Plan for the Future With Sinking Funds

Some expenses don’t happen monthly, but they are guaranteed:

- Holidays

- Car repairs

- School costs

- Gifts

- Home maintenance

Divide those yearly costs by 12 and save a little every month. This turns emergencies into prepared events.

Step Five: Separate Your Spending Into Needs and Wants

This is one of the most powerful mindset shifts you can make.

Needs

Things you must pay to survive:

- Housing 🏠

- Basic food

- Transport

- Utilities

- Minimum debt repayments

Wants

Things that make life enjoyable:

- Eating out

- Streaming services

- New clothes

- Hobbies

- Travel

When money gets tight, you adjust wants not needs. That is how you stay in control.

Step Six: Balance Your Budget

Your expenses must not exceed your income. If they do, reduce spending or increase earnings.

Once your basics are clear, many people switch to a more structured system like this:

- ✔ Organizes finances

- ✔ Improves consistency

- ✔ Great for discipline

If debt is one of your largest expenses, apply a structured debt payoff system to eliminate it faster.

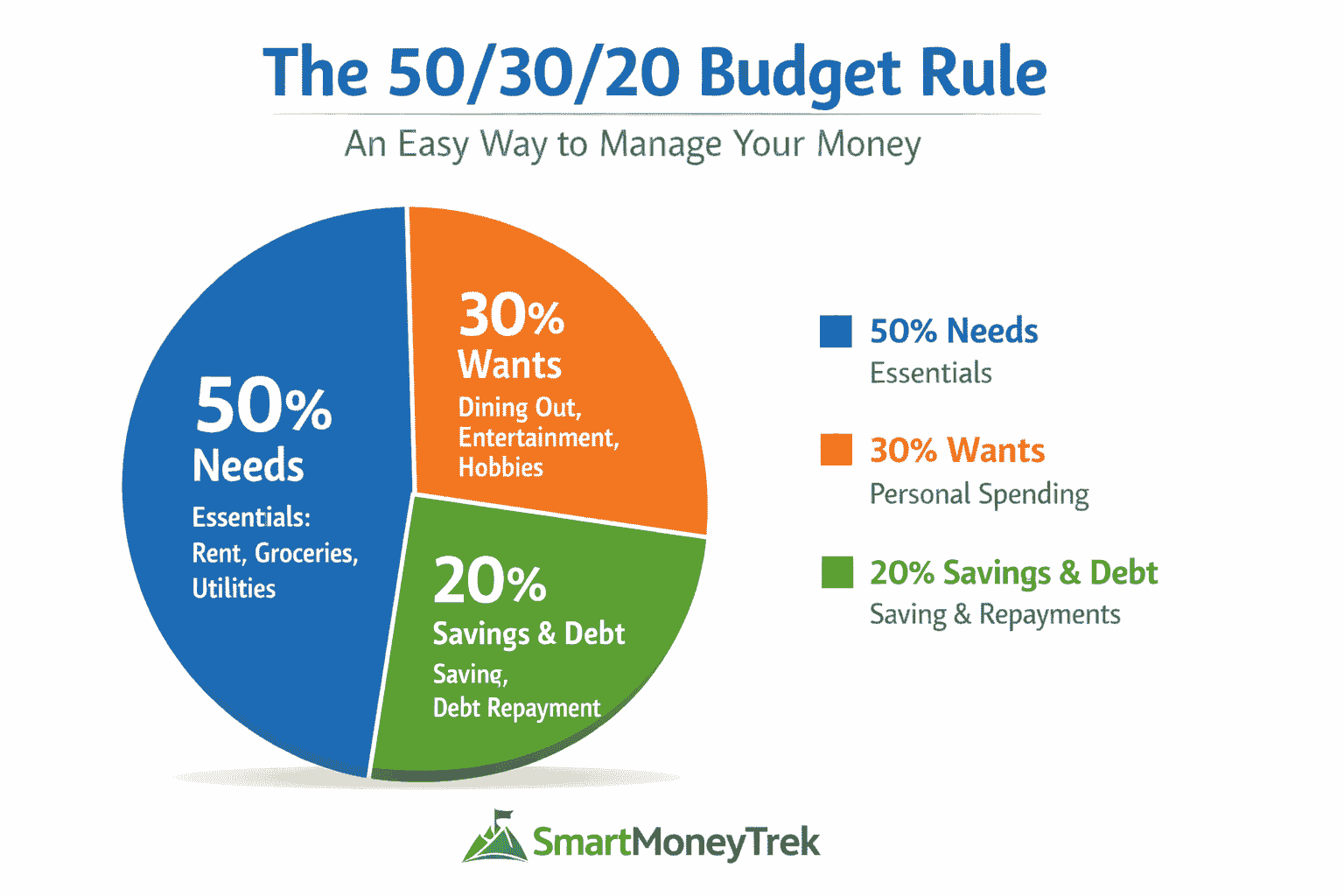

The 50/30/20 Budget Rule (Balanced Framework)

If you want a clean, easy way to budget, this rule works beautifully. This popular budgeting method helps beginners maintain balance:

How the 50/30/20 Budget Rule Works

This visual shows how your income is split between needs, wants, and savings so you can stay balanced and financially safe.

- 50% for needs – Your survival and responsibilities.

- 30% for wants – Your lifestyle and enjoyment.

- 20% for savings & debt – Your future self.

This structure keeps your life balanced. You don’t live in fear. You don’t spend recklessly. You move forward. When your debt is high, you can shift more into the 20% category until it is gone.

If you are dealing with loans or credit cards, visit our how to pay off debt faster without destroying your lifestyle to prioritize repayments correctly.

Free SmartMoneyTrek Budget Worksheet

To help you implement everything in this guide, we created a free printable monthly budget kit.

Get the Free SmartMoneyTrek Budget Kit 👇

Download our professionally designed Ultimate Monthly Budget Kit to track your income, control spending, and start building real savings even on a low income.

- ✔ Monthly income & expense worksheet

- ✔ Step-by-step budgeting instructions

- ✔ Visual budget examples

- ✔ Designed for everyone

100% free. No signup. No spam.

Zero-Based Budgeting: Giving Every Dollar a Job

With this method: Income minus expenses equals zero. That doesn’t mean you spend everything. It means every dollar is assigned to bills, savings, debt, or enjoyment. Money without a job always disappears.

This method is especially powerful if you are trying to pay off debt or build an emergency fund because it forces every dollar to have a purpose.

Digital vs Manual Budgeting: Which Is Better?

Both work. The best one is the one you will actually use.

Digital apps

- Automatic tracking

- Easy reporting

- Convenient

Manual methods

- You feel every purchase

- You become more mindful

- You build stronger habits

The Case for Digital Budgeting Tools

Apps like YNAB (You Need A Budget) or modern AI-integrated budgeting apps can categorize your spending automatically. This is great for busy professionals who just want a "dashboard" view of their life.

There is a psychological "pain" associated with writing down a purchase. If you are a chronic overspender, I recommend a manual budget for at least the first 90 days. When you have to physically type in "$14 for a sandwich," you start to question if the sandwich was really worth the effort.

cut unnecessary expenses effectively Many people start manually and move digital later.

If you're unsure which budgeting method fits you best, this quick comparison helps:

Best Budgeting Tools Compared (Choose What Fits You)

Not sure which budgeting tool to choose? This quick comparison makes it easy to pick the one that matches your style and financial habits.

Budget Planner Notebook

Simple, structured monthly budgeting system for beginners and consistent planners.

- ✔ Easy to follow layout

- ✔ Tracks income & expenses

- ✔ Perfect for long-term use

Cash Envelope System

Best for controlling overspending and building strong money habits fast.

- ✔ Stops impulse spending

- ✔ Physical money control

- ✔ Great for beginners

Complete Budgeting System Kit

All-in-one system for full financial control, organization, and long-term planning.

- ✔ Full budgeting system

- ✔ Tracks everything

- ✔ Long-term financial planning

A Real-Life Example

Here is a simple monthly budget example to show how this works in real life:

Imagine someone earning $4,500 per month. Before budgeting, money runs out, credit cards grow and savings stay empty.

With a simple 50/30/20 plan:

- $2,250 for needs

- $1,350 for wants

- $900 for savings and debt

Within six months:

- Bills are paid

- Fun still exists

- "money anxiety" vanished

- The future is protected

That is what budgeting does. It turns chaos into calm.

How to Stick to Your Budget Long-Term

The secret is not discipline. It is systems.

1. Check in Weekly

Five or ten minutes. Look at what you spent. Adjust if needed.

2. Automate Your Money

Automation works best when paired with simple budgeting systems that you review regularly.

Savings, bills, and debt payments should happen automatically. What you don’t see, you won’t spend. apply a structured debt payoff system

3. Give Yourself Permission to Enjoy Life

A budget that allows joy lasts longer.

4. Never quit after one bad month

Bad months happen. Good money habits are built by returning not quitting, forgive Mistakes

5. Reduce Decision Fatigue

The more financial decisions you automate, the less willpower you consume. Willpower is limited. Systems are not.

When Your Budget Breaks

Budgets will break sometimes. That does not mean you failed.

It means:

- Something changed

- Your numbers need adjusting

- You are learning

If debt or overspending keeps knocking your budget over, visit our debt recovery guides to regain control.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

Common Budgeting Myths That Keep People Broke

Myth 1: Budgeting Means Cutting Everything Fun

A sustainable budget includes enjoyment. The goal is balance, not deprivation.

Myth 2: Budgeting Only Matters If You Are In Debt

Budgeting builds wealth, not just recovery.

Myth 3: You Need High Income To Budget

Budgeting is most powerful when income is limited because every dollar matters more.

Frequently Asked Questions

A common starting point is the 50/30/20 rule, but the best budget is one that fits your actual income and expenses.

Start small. Even a tiny consistent amount builds discipline and momentum. Then work on reducing expenses or increasing income.

The easiest way to start is to list your income, track your expenses, and follow a simple rule like the 50/30/20 budget to stay balanced.

Yes. Budgeting helps you build savings, prepare for emergencies, and grow wealth intentionally.

If you're ready to fully take control of your money, this is the system most people upgrade to:

- ✔ Tracks income, expenses, and savings in one place

- ✔ Helps you stay consistent with your budget

- ✔ Reduces overspending and financial stress

- ✔ Perfect for beginners and serious planners

Final Thoughts: Your Money Should Serve Your Life

A budget is not about being cheap. It is about being intentional.

When you control your money:

- Stress decreases

- Confidence grows

- Possibilities open

If your budget shows little leftover income, consider boosting your monthly income strategically.

Financial freedom does not begin with investing. It begins with clarity. And clarity begins with a monthly budget. You do not need a raise. You do not need perfection. You need structure. Start today. Adjust monthly. Improve consistently. That is how control becomes confidence. And confidence becomes wealth.

This content is for educational purposes only and does not constitute financial advice.