Budgeting Explained: What It Is and How It Works

What Is Budgeting? (Quick Answer)

Budgeting is the process of planning your income and expenses in advance so you can take control of your money, avoid overspending, and consistently build savings.

🚀 Quick Start: Begin Budgeting in Minutes

Follow these simple steps to take control of your money immediately—even if you're starting from scratch.

📘 In This Guide 👇

- What Is Budgeting? (Quick Answer)

- Introduction: Budgeting Isn’t About Money—It’s About Direction

- What Budgeting Really Means

- The Mindset Shift: From Restriction to Permission

- Why Most Budgets Fail Before They Start

- The Psychology of Money: What Drives Your Spending

- Understanding Your Financial Reality

- The Silent Killers of Your Finances

- Cash Flow: The Backbone of Budgeting

- Planning for Imperfection: Managing Irregular Expenses

- The Solution: Sinking Funds

- Defining Your Financial Priorities

- The Role of Goals: Giving Your Budget Direction

- Choosing the Right Budgeting Framework

- Tools vs. Behavior: What Really Matters

- The Pre-Budget Audit: Your Most Important Step

- Proactive vs. Reactive Money Management

- The Role of an Emergency Fund

- The First-Month Reality: Expect Adjustment

- The Power of Consistency

- Conclusion: Budgeting Is a Lifestyle, Not a Task

- Frequently Asked Questions

- Final Thoughts

Introduction: Budgeting Isn’t About Money—It’s About Direction

Budgeting is not about restriction; it’s about direction. Instead of limiting your lifestyle, a good budget gives your money purpose and helps you make confident financial decisions without stress or guilt.

Without a clear plan, money is often spent based on impulse or habit. A structured approach allows you to stay in control, align your spending with your priorities, and build long-term financial stability.

Important: This guide focuses on the mindset and foundation you need before creating a budget, so your system actually works in real life.

If you're ready to build your budget, follow our step-by-step budgeting guide or learn how to create a monthly budget.

Expert Insight: This guide is based on practical budgeting systems, behavioral finance principles, and real-world money management strategies.

What Budgeting Really Means

At its core, budgeting is straightforward:

It is a plan for how you will use your money before it is spent. That’s it, no restriction, no punishment, and it does not need to be complicated.

A budget is best understood as three powerful things at once:

- A decision-making tool — guiding your choices before money leaves your hands

- A financial blueprint — giving structure and direction to your income

- A reflection of your priorities — showing, in clear terms, what truly matters to you

When you approach budgeting this way, everything changes. You stop reacting to your finances after the fact, asking: “Where did my money go?” And instead, you begin to take control upfront, deciding: “Where should my money go?”

That shift from passive tracking to intentional planning is what turns budgeting from a chore into a powerful system for building financial stability and long-term progress.

To see how budgeting works in practice, read our step-by-step budgeting guide.

Simple Budgeting Example

For example, if you earn $1,000 per month:

- $500 for needs

- $300 for wants

- $200 for savings

Best Budgeting Tools for Beginners (Simple & Effective)

If you struggle to stay consistent with budgeting, using a simple physical system can make tracking your money much easier. Below is one of the best tools for beginners:

✔ Visual spending control

✔ Perfect for low income budgeting

Why Budgeting Matters More Than Ever

- Over 60% of people struggle with consistent savings

- Most households operate without a structured budget

- Lack of budgeting is one of the leading causes of financial stress

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people, especially those building stability from limited income.

Saving money works best when you are tracking every dollar with a zero based budget.

The Mindset Shift: From Restriction to Permission

The most common mistake people make is viewing budgeting as a system of limitation. In reality, an effective budget functions as a permission system. It does not tell you what you cannot do; it clearly defines what you can do, with confidence and without regret.

Instead of thinking: “I can’t spend money on enjoyment,” A well-structured budget allows you to say: “I’ve already planned for enjoyment, so I can spend without guilt.” Learn how to build savings from scratch.

This distinction is powerful.

For instance:

- When you allocate a portion of your income to dining or leisure, you can enjoy those experiences freely, because they are already accounted for.

- When your savings and essential obligations are planned in advance, every remaining expense becomes intentional rather than stressful.

This shift in perspective changes everything. A budget does not restrict your lifestyle, it supports it. It ensures that the life you want to live is not only possible, but financially sustainable.

If your income is limited, understanding how to budget effectively on a low income can significantly improve your financial stability.If you don’t yet have a simple tracking system, follow our complete beginner budgeting guide to see where your money is leaking and how to plug those holes.

Why Most Budgets Fail Before They Start

Understanding where budgets typically break down gives you a decisive advantage. Most failures are not caused by a lack of intelligence or effort, but by flawed assumptions at the very beginning.

1. No Clear Purpose (“Why”)

Without a defined purpose, budgeting quickly feels like a burden. A sustainable budget is driven by a clear internal reason, a financial North Star that guides your decisions. You must be able to answer, with clarity:

- Why do I want to budget?

- What do I want my money to accomplish?

Without this foundation, discipline becomes fragile. Motivation fades, and the budget loses its meaning.

2. Focusing Only on Numbers

Many people treat budgeting as a purely mathematical exercise. In reality, budgeting is far more behavioral than numerical.

Your habits, impulses, emotions, and daily decisions have a greater impact than any calculation. A perfectly designed spreadsheet cannot compensate for unexamined spending patterns or inconsistent behavior.

Until you address how you act with money not just how you calculate it, your budget will struggle to hold.

3. Creating an Unrealistic “Ideal Life” Budget

A common mistake is building a budget around an idealized version of yourself rather than your current reality.

You may think:

- “I will completely stop eating out.”

- “I will start saving 50% of my income immediately.”

While these intentions may be admirable, they are often unsustainable. When reality inevitably clashes with these expectations, the budget collapses not because budgeting doesn’t work, but because the plan was never realistic to begin with.

An effective budget meets you where you are, then gradually moves you forward.

4. Expecting Perfection

Many people abandon budgeting after the first mistake, assuming they have failed. But the truth is simple:

Your first budget may be wrong. And that is not a flaw, it is part of the process.

Budgeting is iterative. It improves through adjustment, refinement, and consistency over time. The goal is not perfection from the start, but progress with each revision.

When you understand these failure points early, you stop approaching budgeting as a rigid system to “get right” on the first attempt and start treating it as a flexible tool you refine until it works for your life.

Biggest Budgeting Mistakes to Avoid

- Starting without a clear goal

- Creating unrealistic budgets

- Ignoring spending behavior

- Expecting perfection

If your income is currently limited, consider increasing it with realistic side income ideas for beginners.

The Psychology of Money: What Drives Your Spending

Before numbers, there is behavior, and before behavior, there is psychology. To build a budget that truly works, you must first understand the invisible forces shaping your financial decisions.

a. Emotional Spending Is Real

Spending is rarely just a logical act, it is often an emotional response. People do not simply spend money; they react with it.

You may find yourself spending because:

- You are under stress and seeking relief

- You want comfort or a sense of control

- You wish to feel accomplished or successful

- You are influenced subtly or directly by the people around you

These moments often go unnoticed, yet they are where many budgets quietly begin to fail. Not because the numbers are wrong, but because the underlying triggers remain unaddressed.

b. Common Psychological Traps

Certain patterns of thinking consistently lead to poor financial decisions. Recognizing them is the first step to overcoming them.

* The Status Trap

Spending to impress others rather than to serve your own needs or values. This often leads to short-term validation at the cost of long-term stability.

* The Convenience Trap

Choosing the easier, faster option even when it is more expensive simply because planning feels overwhelming or time-consuming.

* The “Treat Yourself” Cycle

Using spending as a form of reward or escape. While occasional rewards are healthy, repeated reliance on this pattern can quietly erode your finances.

c. Discipline Beats Motivation

Many people rely on motivation to manage their finances, but motivation is inconsistent and short-lived. What sustains progress is not how inspired you feel, but the systems you build.

Budgeting becomes effective when it evolves into:

- A habit — something you do automatically

- A routine — integrated into your regular life

- A system — structured in a way that supports consistency

When discipline replaces dependence on motivation, your financial decisions become steady, intentional, and far more resilient over time.

If you’re starting from zero, read our How to Save Money on a Low Income to build financial security faster.

Quick Question: Do you currently track your spending?

If not, this is the first step to taking control of your finances.

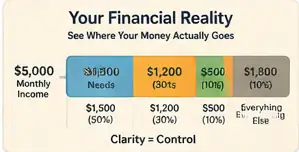

Understanding Your Financial Reality

Before you can plan your financial future with clarity, you must first confront your present with honesty. A strong budget is not built on assumptions, it is built on accurate awareness.

a. Know Your True Income

Clarity begins with understanding exactly what you earn. This includes all reliable sources:

- Your primary salary or wages

- Side hustles or small businesses

- Freelance or contract income

If your income fluctuates, avoid overestimating. Instead, work with a conservative average, a figure you can depend on even in lower-earning periods. This protects your budget from unnecessary strain and reduces financial uncertainty.

For those who have irregular income, budgeting with irregular income to have flexibility needed for effective planning.

b. Track Your Spending (The Reality Check)

Awareness of income alone is not enough, you must also understand where your money actually goes. Commit to tracking every expense for at least 30 days. No assumptions. No omissions.

This process will reveal:

- Hidden expenses that quietly drain your income

- Wasteful habits that go unnoticed in daily life

- Spending patterns you may never have consciously recognized

For many people, this step is transformative. It replaces vague assumptions with concrete insight, turning financial confusion into clarity.

c. Fixed vs. Variable Expenses

Not all expenses are equal. Understanding the difference gives you control.

-

Fixed expenses are predictable and consistent:

Rent, school fees, loan repayments, subscriptions -

Variable expenses fluctuate based on your choices:

Food, transportation, entertainment, lifestyle spending

While fixed costs often feel non-negotiable, it is within your variable expenses that real change happens. These are the areas where small, consistent adjustments can significantly improve your financial position over time.

When you fully understand your financial reality, you move from guesswork to precision. And that clarity becomes the foundation for every effective budgeting decision that follows.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

The Silent Killers of Your Finances

Not all financial threats are obvious. Some do not demand attention, they quietly erode your progress over time. Understanding these subtle patterns is essential if you want to protect and grow your money.

a. “Ghost Expenses”

These are the costs that operate in the background, easy to overlook, yet consistently draining. They include:

- Forgotten subscriptions

- Small, routine purchases

- Automatic renewals you no longer notice

Individually, they seem insignificant. But collectively, they can consume a meaningful portion of your income without your awareness. What makes them dangerous is not their size, but their invisibility.

b. Lifestyle Inflation

As income increases, spending often rises alongside it. What once felt like a luxury gradually becomes a necessity. Upgrades become normal. Comfort becomes expected.

Without deliberate control, higher earnings do not translate into financial progress, they simply fund a more expensive lifestyle. The result? You may earn more, yet remain in the same financial position.

c. The Illusion of Small Spending

Small amounts rarely feel consequential in the moment. A daily expense of $100 may seem harmless. But over time, the impact compounds:

- Over a month: $3,000

- Over a year: $36,000

What appears trivial in isolation can become significant in accumulation. This is the quiet mathematics of money where consistency, not size, determines long-term impact.

These silent financial drains rarely cause immediate alarm, which is precisely why they are so effective. Left unchecked, they can undermine even the best financial intentions. Because in the end, it is often not the large expenses that destabilize your finances, but the small, repeated ones you fail to notice.

If your income is tight, learn realistic ways to increase your income so you can improve your savings rate.Easy Budgeting Systems to Start Managing Your Money

If your money disappears before the month ends, using a simple physical system can make tracking your money much easier. Below is one of the best tools for beginners:

✔ Stops impulse buying

✔ Saves money weekly

Cash Flow: The Backbone of Budgeting

At the heart of every effective budget lies one non-negotiable principle: cash flow.

Cash Flow = Income − Expenses

This simple relationship determines your financial direction at any given time. In practical terms, there are only three possible outcomes:

- You are living within your means — your income exceeds your expenses, allowing room for savings and growth

- You are breaking even — your income and expenses are equal, leaving no margin for progress

- You are overspending — your expenses exceed your income, gradually creating financial strain

Every financial decision you make ultimately feeds into one of these outcomes. Your objective is clear: to build and maintain consistent positive cash flow.

Why? Because positive cash flow is what enables everything else. It is the source of your ability to save, invest, handle emergencies, and create long-term financial stability.

Learn how to control your cash flow using a zero-based budgeting system.

Without it, even the best financial plans collapse under pressure. With it, you gain the flexibility and control needed to move forward with confidence. In essence, cash flow is not just a calculation, it is the foundation upon which your entire financial life is built.

Smart Tools to Control Your Spending and Save More

If you want a simple system that actually works, using this system can make tracking your money much easier. Below is one of the best tools for beginners:

✔ Reduces electricity bills

✔ Works automatically

Planning for Imperfection: Managing Irregular Expenses

Life is inherently unpredictable and a budget that ignores this reality is designed to fail. A truly effective budget does not assume perfect consistency. Instead, it anticipates the unexpected and prepares for it in advance. Irregular expenses are a natural part of life. They do not occur monthly, but when they do, they often demand immediate attention. Common examples include:

- Medical bills

- Vehicle repairs

- School fees

- Festive and seasonal spending

These expenses are not surprises; they are simply infrequent certainties. The mistake many people make is treating them as emergencies, rather than planning for them proactively. As a result, each occurrence disrupts their finances, creating unnecessary stress and instability.

A well-structured budget accounts for these realities by setting aside small amounts over time. This approach spreads the financial impact, making large, occasional expenses manageable rather than overwhelming.

In essence, planning for irregular expenses is planning for real life. Because financial stability is not built on perfect months, it is built on preparation for imperfect ones.

If your income is irregular, check budgeting with irregular income to have effective control of your finances.

The Solution: Sinking Funds

The most effective way to handle irregular expenses is through a simple but powerful strategy: sinking funds.

A sinking fund involves setting aside small, consistent amounts of money each month for expenses you know will arise in the future. Instead of being caught off guard, you prepare in advance gradually and intentionally.

For example:

- Setting aside $1000 per month toward school fees

- Allocating $500 per month for maintenance or repairs

Over time, these contributions accumulate, ensuring that when the expense arrives, the money is already available. The impact of this approach is significant.

What would have felt like a financial emergency becomes a planned, manageable event. Instead of reacting with stress, you respond with readiness. Sinking funds shift your finances from uncertainty to control, allowing you to handle life’s inevitable costs with confidence and stability.

Defining Your Financial Priorities

A budget without clearly defined priorities is nothing more than a collection of numbers: organized, perhaps, but directionless. For a budget to be meaningful, it must be anchored in what truly matters to you. This begins with honest reflection:

- What matters most to me?

- What do I want my money to accomplish?

Your answers form the foundation of every financial decision you make. They give your budget purpose, structure, and direction. For many, these priorities may include:

- Achieving freedom from debt

- Building long-term financial security

- Supporting family and loved ones

- Investing in or growing a business

There is no universal template. What matters is that your budget reflects your values, not external pressure, not societal expectations, and not comparison with others. When your spending aligns with your priorities, your budget becomes more than a plan, it becomes a tool for intentional living. Because ultimately, money is not the goal, it is a resource and its highest value lies in how effectively it helps you build the life you truly want.

The Role of Goals: Giving Your Budget Direction

Without goals, a budget is merely a structure. With goals, it becomes a mission.

Goals give your money purpose. They transform routine financial decisions into intentional steps toward a clearly defined future. Instead of simply managing income and expenses, you begin directing your resources with clarity and focus. To build a balanced and effective financial plan, your goals should span different time horizons:

Short-Term Goals (0–12 months)

These are immediate priorities that strengthen your financial foundation and create stability. Examples include:

- Building an emergency fund

- Clearing small or high-interest debts

Short-term goals provide quick wins, building momentum and confidence in your budgeting process.

Medium-Term Goals (1–5 years)

These goals require planning, discipline, and sustained effort. They often include:

- Starting or expanding a business

- Funding education or skill development

Medium-term goals bridge the gap between your present situation and your larger ambitions.

Long-Term Goals (5+ years)

These define the broader vision for your financial future. Common examples include:

- Achieving financial independence

- Acquiring property or long-term assets

Long-term goals require consistency and patience, but they are the most transformative.

When your budget is aligned with clearly defined goals, every naira you allocate serves a purpose. Spending becomes intentional, saving becomes meaningful, and progress becomes measurable. Because ultimately, a budget is not just about managing money, it is about building a future with direction and clarity.

Make Goals Specific

Instead of: “I want to save money”. Say: “I want to save $30,000 in 6 months”. Clarity drives action.

Types of Budgeting Methods

- 50/30/20 budget

- Zero-based budgeting

- Envelope system

- Pay yourself first

Choosing the Right Budgeting Framework

There is no universal budgeting system only the one that works effectively for you.

A successful framework is not defined by complexity or popularity, but by consistency. The right method is the one you can apply with clarity, maintain with discipline, and adapt to your lifestyle over time. Below are some of the most widely used approaches:

1. The 50/30/20 Rule

A simple and flexible structure that divides your income into three categories:

- 50% for Needs — essential expenses such as housing, food, and utilities

- 30% for Wants — lifestyle choices and discretionary spending

- 20% for Savings and Investments — future-focused financial growth

This method is ideal for those seeking balance without overcomplicating the process.

2. Zero-Based Budgeting

A highly intentional approach where every dollar is assigned a specific purpose. Income minus expenses equals zero not because you spend everything, but because every amount is deliberately allocated, including savings. This method provides maximum control and clarity.

3. The Envelope System

A practical, hands-on method that uses physical cash allocations for different spending categories. Once the money in an envelope is exhausted, spending in that category stops. This creates clear boundaries and strengthens spending discipline.

4. Pay Yourself First

A priority driven system that focuses on saving before spending. A portion of your income is set aside immediately for savings or investments, and you then manage your expenses with what remains. This ensures that your future is consistently funded.

Each of these frameworks offers a different path, but the destination is the same: control, clarity, and financial progress. Ultimately, the most effective budgeting system is not the most sophisticated, it is the one you will use consistently and refine over time.

| Method | Best For | Difficulty |

|---|---|---|

| 50/30/20 Rule | Beginners | Easy |

| Zero-Based Budget | Full control | Medium |

| Envelope System | Overspenders | Easy |

| Pay Yourself First | Savers | Easy |

Practical Budgeting Tools That Actually Work for Beginners

If tracking your expenses feels overwhelming, using a simple physical system can make tracking your money much easier. Below is one of the best tools for beginners:

✔ Builds money discipline

✔ Simple and effective system

Tools vs. Behavior: What Really Matters

It is easy to assume that the right app or tool will solve your financial challenges. No, it won’t. Tools can support your efforts, but they do not create results. Behavior does.

Wealth is not built through sophisticated software; it is built through consistent, disciplined action over time. You can manage your finances effectively with the simplest tools:

- A notebook

- A basic spreadsheet

- Even the notes app on your phone

What matters is not the tool itself, but how consistently you use it. A well-designed app cannot compensate for inconsistency, just as a simple system can produce powerful results when applied with discipline.

In the end, success in budgeting is not determined by complexity, it is determined by commitment. Because consistency, applied daily, will always outperform complexity that is rarely sustained.

The Pre-Budget Audit: Your Most Important Step

Before you create a budget, you must first understand your financial landscape in full. This is where the pre-budget audit becomes essential. It is the process of bringing clarity to your money, replacing assumptions with facts, and confusion with structure. Without this step, any budget you create is built on incomplete information. A proper audit requires deliberate attention to the following:

. Gather your financial records

Collect bank statements, receipts, bills, and any documents that reflect your financial activity. This forms the foundation of accurate analysis.

. List all income sources

Identify every stream of income—primary earnings, side hustles, freelance work, and any irregular inflows.

. Track all expenses

Account for every outgoing amount, no matter how small. Precision here is critical.

. Categorize your spending

Organize expenses into clear groups such as needs, wants, and savings. This reveals how your money is distributed.

. Identify financial leaks

Look for patterns of unnecessary or unnoticed spending those small, repeated costs that quietly drain your resources.

This process may seem simple, but its impact is profound. A pre-budget audit does more than prepare you to create a budget, it gives you a clear, honest picture of your financial reality, and with that clarity, you are no longer guessing, you are making informed, intentional decisions. Because the strength of your budget is determined long before you create it.

Proactive vs. Reactive Money Management

Most people manage their money reactively.

They look backward, tracking what has already been spent, trying to make sense of decisions after the fact. By then, the money is gone, and control is limited.

In contrast, effective budgeters operate proactively.

They look forward, deciding in advance how their money will be used, assigning purpose to every amount before it is spent. Each expense is intentional, not accidental.

This distinction is fundamental.

Reactive money management leaves your finances vulnerable to impulse, pressure, and uncertainty. Proactive money management creates structure, clarity, and direction.

In essence, it is the difference between: Responding to your money and directing your money. Between uncertainty and intention. Between chaos and control.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

The Role of an Emergency Fund

Without a financial buffer, even the best budget remains vulnerable. An emergency fund is what gives your financial plan resilience, the ability to withstand unexpected events without collapsing under pressure. Because the reality is simple: life is unpredictable. A single unplanned expense can:

- Disrupt your entire budget

- Push you into unnecessary debt

- Force you to start over financially

This is not a failure of budgeting, it is a lack of protection.

An emergency fund acts as that protection. It creates a layer of stability between you and life’s uncertainties, allowing you to respond calmly rather than react under pressure.

A practical starting point is to build savings equivalent to 1 to 3 months of essential expenses. This initial buffer may seem modest, but its impact is significant. It provides breathing room, reduces financial stress, and strengthens your ability to stay consistent with your plan.

Over time, this foundation can be expanded, but even the first step changes everything. Because true financial control is not just about planning for the expected, it is about being prepared for the unexpected.

The First-Month Reality: Expect Adjustment

Your first budget will not be perfect and it is not meant to be. This initial phase is not about getting everything right; it is about learning how your financial life actually works. Every adjustment you make brings your budget closer to accuracy and sustainability.

What to Expect

In your first month, you will likely encounter:

- Overspending in certain categories — areas where your initial estimates were too optimistic

- Underestimated expenses — costs that were overlooked or misjudged

- Frequent adjustments — ongoing refinements as real data replaces assumptions

These are not signs of failure. They are evidence that your budget is becoming more aligned with reality.

What to Do

To navigate this phase effectively:

- Review your budget weekly — stay aware and catch issues early

- Adjust your allocations monthly — refine based on actual spending patterns

- Stay consistent — continue the process, even when it feels imperfect

Budgeting is not a one-time setup, it is an evolving system. The goal is not immediate perfection, but continuous improvement. Because in the long run, progress, not perfection is what creates lasting financial success.

The Power of Consistency

Budgeting is not a one-time action, it is a system you sustain. Its effectiveness is not determined by how well you start, but by how consistently you continue. Like any meaningful discipline, the results are built over time, not in a single moment.

Consider it in the same light as personal health, you do not exercise once and expect lasting results. Progress comes from repetition, commitment, and steady effort. The same principle applies to your finances.

When you practice budgeting consistently, you develop:

- Awareness — a clear understanding of where your money goes

- Control — the ability to make intentional financial decisions

- Financial growth — gradual, compounding progress over time

Consistency transforms budgeting from a task into a habit and from a habit into a reliable system that supports your long-term goals. Because ultimately, it is not what you do occasionally that shapes your financial future, but what you do consistently.

Conclusion: Budgeting Is a Lifestyle, Not a Task

Before you begin budgeting, it is essential to understand one fundamental truth: Money is not merely a financial tool, it is a life tool. How you manage it shapes not only your bank account, but the quality, direction, and possibilities of your life.

Budgeting, therefore, is not a restrictive exercise. It is not about:

- Saying “no” to everything you enjoy

- Tracking every kobo with rigid intensity forever

- Living a constrained or deprived life

At its core, budgeting is about something far more meaningful:

- Aligning your money with your values — ensuring your spending reflects what truly matters to you

- Creating intentional freedom — giving yourself permission to spend, save, and invest with clarity and confidence

- Building a future you can influence and control — rather than leaving it to chance

When approached this way, budgeting stops being a task you perform and becomes a lifestyle you live. A lifestyle defined not by restriction, but by purpose, direction, and the quiet confidence that comes from knowing your money is working for you not against you.

Where This Guide Fits in Your Financial Journey

- You are here: Understanding budgeting

- Next: Learn how budgeting works

- Then: Create your first budget

Frequently Asked Questions

Budgeting is simply a plan for how you will use your money before you spend it. It helps you decide where your income should go so you can cover your needs, save for the future, and still enjoy your life without financial stress.

Budgeting is important because it gives you control over your money. Without a budget, it’s easy to overspend, fall into debt, or lose track of your finances. A simple budget helps you build savings, reduce stress, and make better financial decisions.

You can start budgeting on a low income by focusing on your essentials first, tracking every expense, and cutting unnecessary spending. Even small savings matter. The goal is not how much you earn, but how well you manage what you have.

There is no one-size-fits-all method, but popular beginner-friendly options include the 50/30/20 rule, zero-based budgeting, and the envelope system. The best method is the one you can follow consistently.

Most budgets fail because they are unrealistic, too restrictive, or ignore real-life spending habits. Many people also expect perfection and give up after small mistakes. A successful budget is flexible and improves over time.

A common guideline is to save at least 20% of your income, but this may vary based on your situation. If that’s not possible, start with what you can even 5–10%—and increase gradually over time.

An emergency fund is money set aside for unexpected expenses like medical bills, repairs, or job loss. It protects you from going into debt and helps you stay financially stable during difficult situations.

You can start seeing improvements within the first month, especially in awareness and control. However, real financial progress builds over time through consistency, discipline, and regular adjustments.

Still have questions? Explore more guides in our budgeting section.

Final Thoughts

Resist the urge to rush into creating a budget. Instead, take the time to build a solid foundation:

- Understand your habits — recognize how and why you spend

- Define your priorities — be clear about what truly matters to you

- Face your financial reality — assess your income, expenses, and patterns with honesty

This deliberate preparation is what gives your budget strength and direction. Because when you finally begin with clarity, purpose, and self-awareness you move beyond simply organizing numbers; you step into control. You don’t just manage your money. You master it.

👉 Spending too much on food → Meal Planner

👉 High electricity bills → Power Strip

👉 Overspending habits → Envelope System

Start Taking Control of Your Money Today

Don’t wait until your finances become overwhelming. Follow our step-by-step system to create a working budget today.

Create Your First Budget Now →Your financial journey doesn’t need to begin with perfection. It simply needs to begin with consistency, because consistent action, over time, is what turns small steps into lasting progress.

Why This Guide Works:

- Based on real financial behavior (not theory)

- Focused on practical, real-life application

- Designed for long-term consistency not quick fixes

This content is for educational purposes only and does not constitute financial advice.