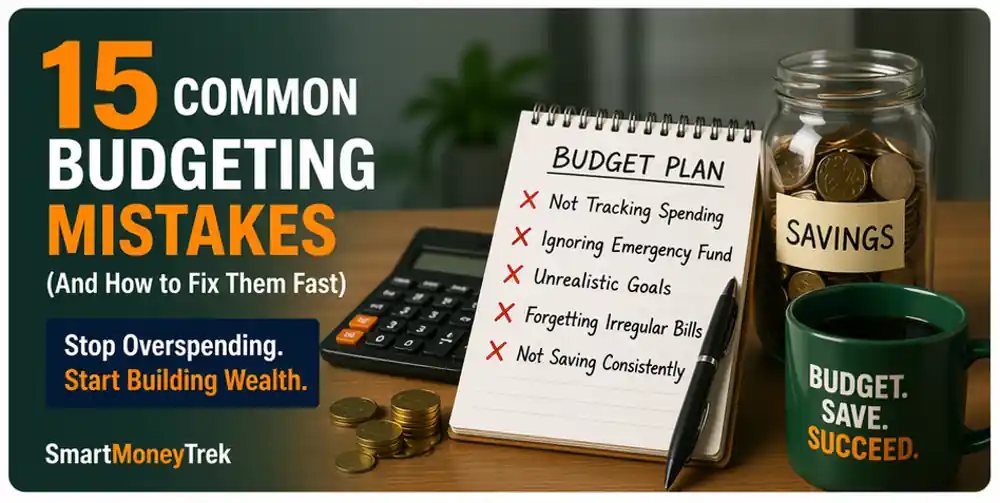

15 Budgeting Mistakes and How to Fix Them

Why do most budgets fail and what should you do differently?

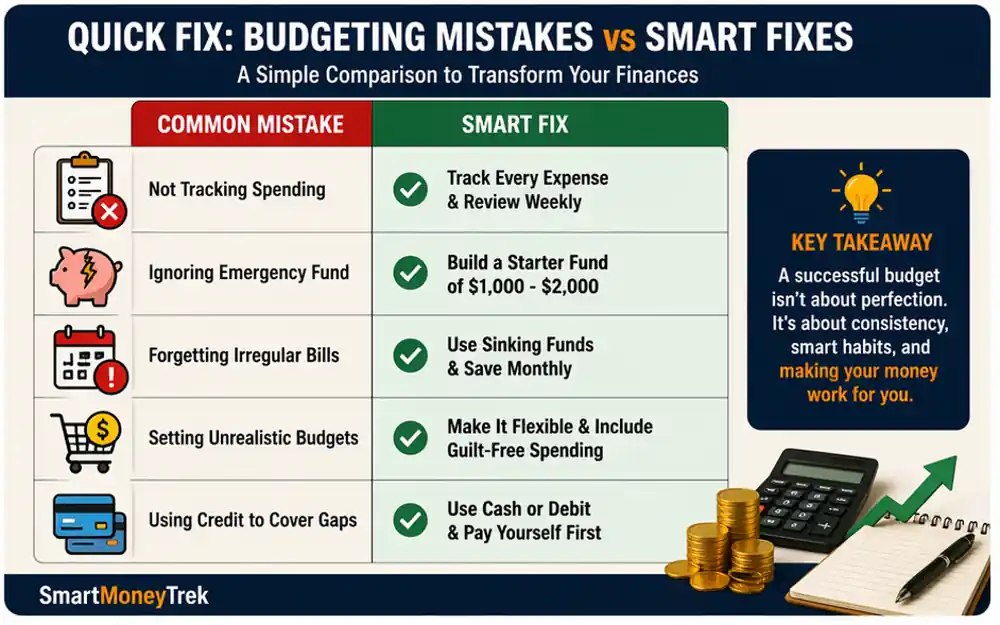

Most budgets fail because of hidden mistakes like unrealistic spending limits, lack of tracking, and no plan for unexpected expenses. These issues make it difficult to stay consistent. The solution is to build a flexible budget, track your spending regularly, and prioritize saving before spending to maintain full control of your finances.

📘 In This Guide 👇

- Why Your Budget Isn’t Working (And How to Fix It Fast)

- 1. Not Having a Clear Budget System

- 2. Not Tracking Your Spending Consistently

- 3. Underestimating Expenses

- 4. Ignoring Small, Everyday Expenses

- 5. Forgetting Irregular Expenses

- 6. Not Having an Emergency Fund

- 7. Setting Unrealistic Budget Goals

- 8. Mixing Wants and Needs

- 9. Saving What’s Left Instead of Paying Yourself First

- 10. Misusing Credit Cards to Cover Budget Gaps

- 11. Failing to Plan for Debt Repayment

- 12. Relying Too Much on Willpower

- 13. Overcomplicating Your Budget

- 14. Not Communicating About Money (For Couples or Families)

- 15. Giving Up After a Bad Month

- Powerful Strategies to Make Your Budget Work

- Frequently Asked Questions

- Final Thoughts: Keep Budgeting Simple and Sustainable

Why Your Budget Isn’t Working (And How to Fix It Fast)

If your budget keeps failing, it’s not because budgeting doesn’t work — it’s because of specific mistakes that quietly break your system.

Most people follow a budget, but still overspend, run out of money, or feel stuck. The issue isn’t effort — it’s hidden errors in how the system is applied.

This guide shows you exactly what’s going wrong and how to fix each mistake so your budget actually works in real life.

If you don’t have a working system yet, start here: how to use a simple monthly budgeting system

At SmartMoneyTrek, we focus on practical personal finance systems designed for real people, especially those building stability from limited income.

✔ Beginner-friendly layout

✔ Helps build consistent habits

✔ Trusted by thousands • ✔ Highly rated • ✔ Beginner-friendly

1. Not Having a Clear Budget System

The mistake:

Managing your finances without a defined budgeting system relying on guesswork or mental tracking instead of a structured plan.

Why it hurts:

Without a clear system, your spending becomes reactive, not intentional. Money slips through unnoticed, leading to poor expense tracking and consistent overspending.

How to fix it:

Use a structured budgeting method like zero-based budgeting, where every dollar is assigned a purpose before the month starts. Whether you choose a budgeting app, spreadsheet, or notebook, the goal is simple: total visibility and control over your money.

Saving money works best when you are tracking every dollar with a zero-based budgeting

2. Not Tracking Your Spending Consistently

The mistake:

Setting a budget but failing to monitor your actual spending.

Why it hurts:

Without consistent expense tracking, your budget becomes ineffective. You lose visibility, making it easy to overspend and miss financial targets.

How to fix it:

Track your expenses regularly, ideally weekly to stay aligned with your budget. Consistent tracking improves awareness, strengthens spending control, and helps you adjust before small issues become bigger problems.

If your fixed expenses feel too high, learn how to reduce expenses and free up cash flow.

3. Underestimating Expenses

The mistake:

Using unrealistic, low estimates when planning your budget to make it seem easier to manage.

Why it hurts:

Inaccurate expense estimates lead to consistent overspending, budget shortfalls, and the false impression that your budget isn’t working.

How to fix it:

Build your budget using real spending data. Review past bank statements and categorize your expenses accurately. Then add a small buffer to each category to improve accuracy and prevent overspending.

4. Ignoring Small, Everyday Expenses

The mistake:

Overlooking minor daily expenses like snacks, transport, or quick online purchases.

Why it hurts:

Frequent small expenses accumulate over time, leading to unnoticed cash leakage and reduced savings.

How to fix it:

Track all expenses—no matter how small. Consistent expense tracking helps you identify spending patterns, eliminate waste, and maintain full control of your budget.

If you’re starting from zero, read our guide to building savings from zero to strengthen your financial foundation.

5. Forgetting Irregular Expenses

The mistake:

Failing to account for non-monthly or irregular expenses in your budget.

Why it hurts:

When these expenses arise, they disrupt your budget and feel like unexpected financial emergencies.

How to fix it:

Plan ahead by creating sinking funds. Break down annual or irregular costs into manageable monthly contributions to stay prepared and maintain budget stability.

For those who prefer more precision and control, how to reduce debt and lower interest costs assigns every dollar a specific purpose.

High monthly bills often lead to debt. If that’s your situation, visit our how to reduce debt and stop high interest payments eating your income.

If your budget keeps failing, it’s not because budgeting doesn’t work — it’s because the system you’re using doesn’t match your spending behavior.

6. Not Having an Emergency Fund

The mistake:

Operating without an emergency fund or financial safety net.

Why it hurts:

Unexpected expenses; medical bills, repairs, or income loss can quickly derail your budget and push you into debt.

How to fix it:

Build an emergency fund starting with a small, achievable target, then gradually grow it to cover 3–6 months of living expenses. Make it a core part of your financial plan, not an afterthought.

If your income is tight, learn ways to increase your income and fix budget gaps so you can improve your savings rate.

7. Setting Unrealistic Budget Goals

The mistake:

Creating an overly restrictive budget that cuts out all discretionary spending.

✔ Easy category-based budgeting

✔ Perfect for discipline and control

✔ Trusted by thousands • ✔ Highly rated • ✔ Beginner-friendly

Why it hurts:

Unrealistic budgeting leads to burnout, reduced consistency, and impulsive “revenge spending” that breaks your plan.

How to fix it:

Build a balanced budget by including a guilt-free spending category (around 5–10% of your income). A sustainable budget is more effective than a perfect but unmaintainable one.

8. Mixing Wants and Needs

The mistake:

Classifying non-essential expenses as necessities within your budget.

Why it hurts:

This misclassification inflates essential spending, reduces financial flexibility, and limits your ability to save or invest.

How to fix it:

Clearly separate and prioritize your expenses:

- Needs: rent, food, utilities

- Wants: dining out, subscriptions, entertainment

Maintain strict boundaries between these categories to improve spending decisions and protect your savings.

9. Saving What’s Left Instead of Paying Yourself First

The mistake:

Treating savings as an afterthought, only saving what remains after spending.

Why it hurts:

This approach leads to inconsistent savings and, in most cases, little or no money set aside.

How to fix it:

Adopt a “pay yourself first” strategy. Automate your savings and treat it as a fixed expense deducted at the start of your income cycle.

To make this automatic, use a structured system like zero-based budgeting so every dollar is assigned before you spend it.

10. Misusing Credit Cards to Cover Budget Gaps

The mistake:

Using credit cards to cover overspending or fill gaps in your budget.

Why it hurts:

This habit turns short-term cash flow issues into long-term debt, often with high interest costs.

How to fix it:

Limit spending in problem categories by using cash or a debit card. Only use credit cards when you can pay the full balance each month to avoid interest and maintain financial control.

11. Failing to Plan for Debt Repayment

The mistake:

Relying on minimum payments without a clear debt repayment strategy.

Why it hurts:

Minimum payments extend your repayment timeline and increase total interest, keeping you in debt longer.

How to fix it:

Use a structured repayment method:

- Debt snowball: focus on clearing the smallest balances first

- Debt avalanche: prioritize debts with the highest interest rates

Choose one approach and stay consistent to accelerate debt payoff.

12. Relying Too Much on Willpower

The mistake:

Depending solely on self-discipline to manage spending habits.

Why it hurts:

Willpower is inconsistent, especially during stress or impulse-driven moments, leading to poor financial decisions.

How to fix it:

Build systems that support better financial behavior:

- Remove spending triggers

- Set spending limits and alerts

- Automate key decisions like saving and bill payments

Make smart money choices easier and more consistent.

13. Overcomplicating Your Budget

The mistake:

Using overly complex budgeting systems that are difficult to maintain consistently.

Why it hurts:

Complexity leads to inconsistency. When a budget is hard to manage, you’re more likely to abandon it altogether.

How to fix it:

Simplify your approach with a proven framework like the 50/30/20 rule:

- 50% Needs

- 30% Wants

- 20% Savings and debt repayment

A simple, sustainable budgeting system delivers more consistent and effective results.

If your system feels too complex, switch to a simpler structure like budgeting on a low income with simple categories to stay consistent.

14. Not Communicating About Money (For Couples or Families)

The mistake:

Managing shared finances without clear communication or joint planning.

Why it hurts:

Lack of alignment on spending, goals, and priorities often leads to conflict, inconsistent decisions, and overspending.

How to fix it:

Schedule regular financial check-ins. Discuss your budget, align on financial goals, and set clear spending limits to ensure accountability and consistency.

15. Giving Up After a Bad Month

The mistake:

Abandoning your budget after a setback or one month of poor performance.

Why it hurts:

Interrupting your efforts disrupts consistency, the primary force behind sustained financial growth, and erodes the momentum you have built over time.

How to fix it:

Adopt a flexible, growth focused approach:

- Adjust budget categories as needed

- Learn from spending mistakes

- Stay consistent and keep moving forward

One difficult month doesn’t define your financial success; your consistency is what matters.

Powerful Strategies to Make Your Budget Work

Fixing budgeting mistakes is essential, but building a reliable system is what drives consistent, long-term financial results.

✔ Focus on Cash Flow Management

Effective budgeting goes beyond expense tracking. It’s about actively directing income toward priorities like savings, debt repayment, and essential spending.

✔ Build Flexibility into Your Budget

Your financial plan should adapt to changes in income, expenses, and lifestyle. A flexible budget is easier to maintain and more resilient.

✔ Leverage Automation

Automate savings, bill payments, and investments to reduce manual effort, avoid missed payments, and improve consistency.

If you struggle with consistency, combine automation with proper expense tracking to stay fully in control.

✔ Review and Adjust Regularly

Treat your budget as a dynamic tool. Conduct monthly reviews to optimize spending, update goals, and stay aligned with your financial plan.

✔ Track and Celebrate Progress

Recognizing small financial wins reinforces positive habits and builds momentum toward larger financial goals.

Best Budgeting Methods Compared (Find What Works for You)

Choosing the right budgeting system can make or break your financial progress. Here’s a simple comparison of the most effective budgeting methods to help you decide quickly.

| Budgeting Method | Best For | Difficulty | Control Level | Key Benefit |

|---|---|---|---|---|

| Zero-Based Budget | Full financial control | Medium | ⭐⭐⭐⭐⭐ | Every dollar has a purpose |

| 50/30/20 Rule | Beginners | Easy | ⭐⭐⭐ | Simple and flexible structure |

| Cash Envelope System | Overspenders | Easy | ⭐⭐⭐⭐ | Prevents impulse spending |

| Digital Budget Apps | Automation lovers | Easy | ⭐⭐⭐ | Tracks spending automatically |

| Budget Planner Notebook | Beginners & consistency | Easy | ⭐⭐⭐⭐ | Builds strong money habits |

Want a simple way to start immediately? Use a beginner-friendly budgeting planner to track your income and expenses consistently.

💡 Quick Tip: If you're just starting, use the 50/30/20 rule. If you want maximum control and faster results, switch to a zero-based budget.

Learn More on SmartMoneyTrek

Explore our core financial guides:

- Save Money – proven ways to cut bills and build savings

- Budgeting – Tools and strategies to control your money

- Make Money – real side hustles and income ideas

- Loans & Debt – How to borrow wisely and eliminate debt

How to Fix a Budget That Doesn’t Work

- Use a system that assigns every dollar

- Track your expenses weekly

- Adjust categories based on real spending

- Cut unrealistic expectations

If your budget keeps failing, switch to a structured system like this method and apply it consistently.

Frequently Asked Questions

The biggest mistake is not tracking spending. Without tracking, you lose control of your money and overspending becomes inevitable.

Most budgets fail because they are unrealistic, too restrictive, or not adjusted over time. Consistency and flexibility are key to success.

Start by tracking all expenses, cutting unnecessary costs, building a small emergency fund, and automating your savings to stay consistent.

The 50/30/20 rule is one of the best methods for beginners because it is simple, flexible, and easy to maintain.

A good target is at least 20% of your income, but you can start smaller and increase gradually as your income grows.

You should review your budget weekly to track spending and monthly to adjust for changes in income or expenses.

Both work well. Cash helps control overspending, while digital tools offer automation and convenience. Choose what fits your habits.

✔ Organizes all finances

✔ Ideal for long-term planning

✔ Highly rated • ✔ Great for long-term budgeting success

Final Thoughts: Budgeting Is About Behavior, Not Just Numbers

Budgeting isn’t just a financial exercise, it’s a system of habits and decision-making.

Long-term success doesn’t come from perfect spreadsheets. It comes from consistency, adaptability, and building systems that support better financial behavior.

When you eliminate these 15 budgeting mistakes and apply the right strategies, your budget becomes more than a plan, it becomes a reliable tool for managing money, reducing stress, and achieving your financial goals.

The key principle is simple:

A budget doesn’t restrict your lifestyle, it gives you control over your money.

Start with a simple system, stay consistent, and refine it as your income and priorities evolve. That’s how sustainable financial progress is achieved.

Ready to Fix Your Budget for Good?

Apply a simple budgeting system step by step and start organizing your income today. Create Your Monthly Budget

Your financial journey doesn’t need to begin with perfection. It simply needs to begin with consistency, because consistent action, over time, is what turns small steps into lasting progress.

This content is for educational purposes only and does not constitute financial advice.